Nordic Credit Rating (NCR) applies a score of 'a-' for the Swedish banking market and views the domestic operating environment as stable. Swedish banks have outperformed most international peers in recent years due to steady lending growth and increased margins. Sweden's economy has been spurred by significant construction activity to address a material housing shortage and accommodate the growing population. However, we expect rising interest rates and a recalibration of housing prices to reduce the pace of capital investment and weigh on economic growth over the next two years. The banking market score is a component of NCR’s issuer ratings for financial institutions. Depending on the nature of the rated entity’s exposure and geographic profile, the score can affect up to 20% of an issuer’s overall credit rating.

“Despite uncertainty around future housing prices, the Swedish banking market continues to perform well”, says Sean Cotten, Lead Analyst for financial institutions at NCR, and adds “competition is increasing for the incumbent banks, but, generally, the banks remain positive outliers in terms of capital, earnings and loss performance among global peers.”

Swedish GDP growth is expected to be 2.9% for 2018, fuelled by low interest rates, a weak currency, strong exports, an expansionary fiscal policy, high immigration and still-high investments in housing and construction. However, there are expectations for lower growth of 2% and 1.8% in 2019 and 2020, respectively, as housing investments drop from peak levels. Consequently, unemployment is expected to fall to 6.1% in 2019 before rising slightly. NCR expects the current low interest environment to persist in the coming years, with the Swedish repo rate remaining below zero until the latter half of 2019 and growing steadily thereafter.

Sweden's banks demonstrate strong performance in key areas. The banks have high regulatory capital ratios, providing valuable capital flexibility and affording large dividend payments to shareholders. The banks have also demonstrated improved earnings and efficiency as margins on mortgage lending have steadily increased and automation and customer behaviour have allowed for significant cost savings, smaller branch networks and reduced staffing even as volumes and revenues rise. Finally, Sweden continues to stand out among European peers with respect to asset quality and loss performance, allowing for efficiency gains to be passed through to shareholders. Looking ahead, NCR expects that margin pressure from existing and newly started competitors could affect banks' future earnings from mortgage lending as interest rates begin their rise towards normality.

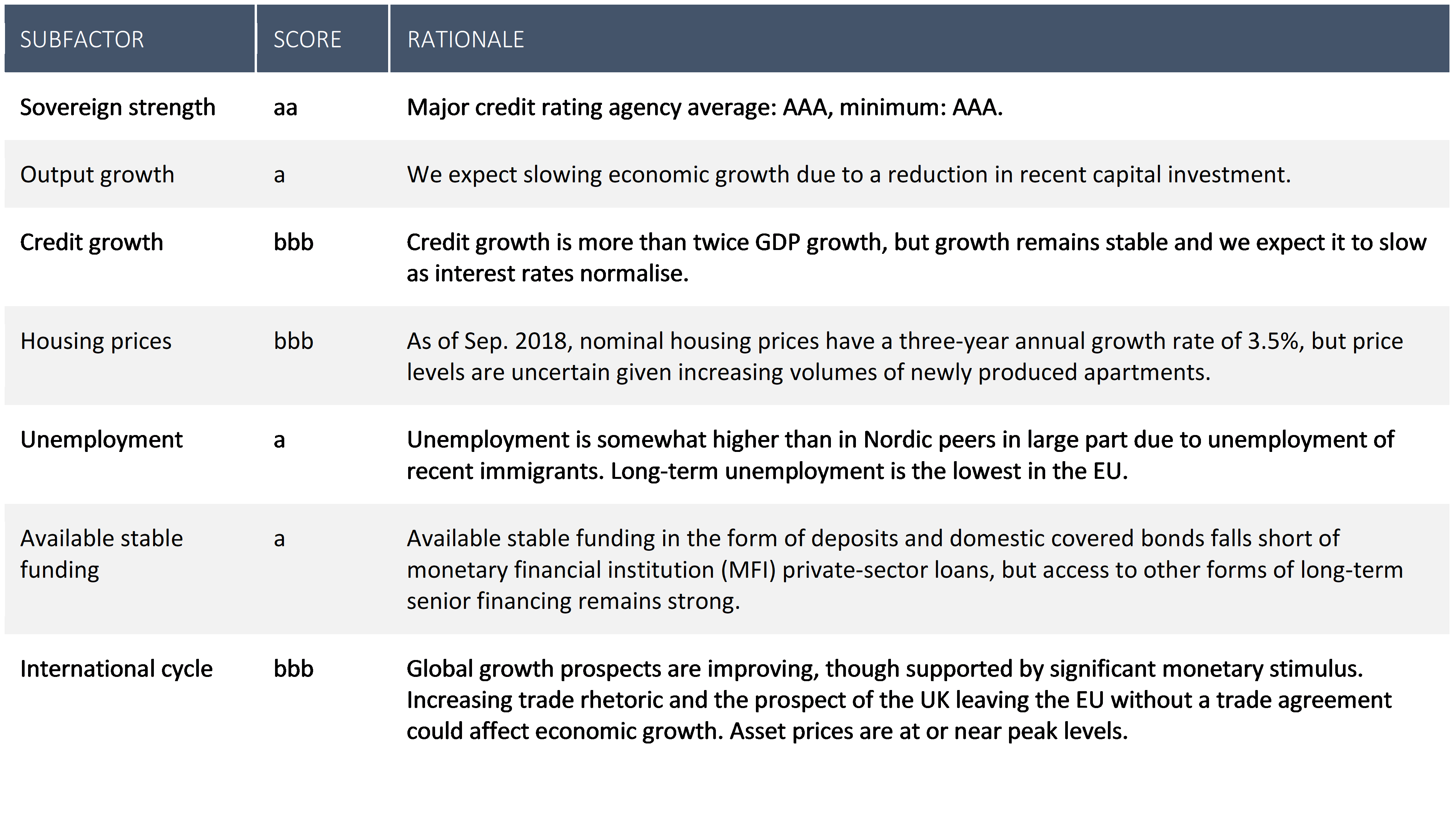

Sweden – scoring of national indicators

If you have any questions, please contact:

Sean Cotten, Lead analyst, +46 732 32 43 78, sean.cotten@nordiccreditrating.com

Geir Kristiansen, Analyst, +47 90 78 45 93, geir.kristiansen@nordiccreditrating.com